The European plastics industry is tackling challenges on multiple fronts. In packaging, by far its biggest market, it has become a victim of its own success, particularly as the ideal material for single-use applications and people on the move. In building and construction, some infrastructure projects may go on hold as governments divert some funds away from infrastructure projects to defence, although business is being boosted as consumers get help to improve energy efficiency in their houses. In automotive, component suppliers are suffering because car makers have been cutting production – not as a reaction to reduced demand, but because they cannot obtain the chips they need for their electronics.

Since early 2019, COVID-19 has had major effects on production, occasionally positive but mostly negative. And now, just as Europe and the rest of the world was recovering from the devastating two years of the pandemic, we have the tragedy of the Ukraine conflict.

Discussing the situation in late March, Martin Wiesweg, Executive Director Polymers EMEA at consultant IHS Markit, said that, quite apart from causing a humanitarian disaster, the crisis is weighing heavy on the plastics business, in terms of cost inflation, the worsening of supply chain bottlenecks, including energy supply, while also raising the spectre of demand shock amid the fear of global stagflation.

Inflation across the EU hit an all-time high of 7.5% in March. S&P Global Economics said on March 30 that it expects eurozone growth to be 3.3% this year, compared to 4.4% in a previous forecast, and inflation to reach 5% this year and stay above 2% in 2023.

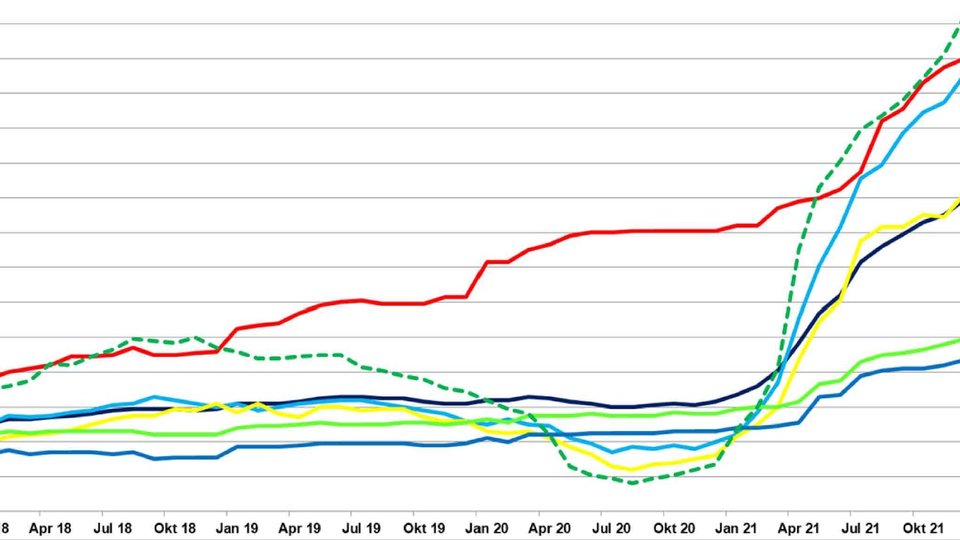

“In the past, high crude oil prices weighed negatively on European plastic demand (see chart) ,” says Wiesweg. Prices soaring further could see consumer disposable income slumping, impacting retail sales. Sectors driven by consumer discretionary income like white goods, consumer products, and automotive would fare poorly as buyers try to conserve cash. “In the short to medium term, Europe could potentially see a demand contraction across polymers.”

Plastics processing is on course for the circular economy

Germany remains the powerhouse of the European plastics industry, with its multiple strengths in materials, equipment, and processing capability. But some sectors are hurting all the same. According to German plastics processing industry umbrella organisation GKV, industry sales increased by 12.6% to €69.4 billion in 2021, but member companies remain under a lot of pressure to produce good results. It cites “exorbitant cost explosions” for raw materials and energy, as well as the many delivery delays and resulting order suspensions, particularly in automotive supplies.

The automotive sector has provided a unique set of problems. Several European car makers have temporarily shut down production in recent months, with important negative effects in the supply chain, including the permanent closure at some processors. Passenger car registrations fell by 2.4% in 2021 to just below 10m units across the 27-country EU, according to the European Automobile Manufacturers Association, ACEA. Jincy Varghese, demand analyst at ICIS, forecasts EU automotive output to grow 17% in 2022, although it will still be down 26% from 2019 levels. A healthy recovery is only likely in the second half, she said in February.

The overall economic outlook for 2022 remains very mixed, said GKV president Roland Roth at the association’s annual results conference in early March. Around half of association members expected sales growth when poled in the run-up to the conference, but a good quarter expected further falls. Several were thinking about relocating or terminating production.

Roth called for a reduction in government surcharges on energy prices. As for material prices, he said recent increases have been “almost insane.” On average, prices for plastics in Europe increased by more than 50% year-on-year in the first half of 2021 and have stayed high. In February 2021, for example, virgin PET sold for around €1/kg. In March of this year, the price was around €1.7/k. Linear low density PE went from around €1.2/kg to around €1.9 over the same period.

But the GKV President remains optimistic: "In 2022, as plastics processors, we will continue to get the best out of polymer materials and successfully complete the tasks ahead,” he said.

Alarm bells have been ringing over energy prices at Unionplast, which represents Italian plastics processing companies. "The crisis in energy prices is seriously affecting a sector that has over 5,000 companies, and more than 100,000 employees," says Marco Bergaglio, President of the association.

"The uncontrolled increase in energy costs and the growing difficulty in finding raw materials is a deadly mix for our sector and creates the real risk of not being able to meet the demands of our customers. This situation has inevitable consequences also on the prices of our products.”

Some car makers cannot build cars because they are unable to obtain chips for electronics. This has had a knock-on effect upstream, putting some plastics component suppliers in difficulties. (Photo, Getty Images)