The European plastics industry faces challenges from strict regulations, rising recycling demands, and record-high energy costs. Production is shifting outside the EU, risking dependence on imports and weakened competitiveness. While recycling is vital, cheaper, lower-quality imports threaten local processors. To safeguard jobs and competitiveness, the sector needs stable regulations, fair recycling policies, and lower energy costs.

The plastics processing industry in Poland and across the European Union is currently facing serious challenges which directly affect its competitiveness, stability and future growth prospects. Companies in the sector are increasingly impacted by both regulatory and economic factors.

On the one hand, firms must contend with increasingly restrictive EU regulations, which impose additional administrative and technological requirements; on the other, growing pressure to raise recycling rates is forcing costly investment in new solutions and processes. Added to this are record-high energy prices, which significantly increase production costs and reduce profitability. As a result, European firms are at risk of losing their competitive edge to manufacturers outside the EU, where regulations are less stringent and production costs considerably lower.

Over-regulation and the risk of losing production from Europe

In recent years, the EU plastics sector has been burdened with another wave of environmental, production and trade regulations. While many of these are justified on environmental grounds, their excessive pace of introduction combined with other adverse factors means that the production of virgin plastics is gradually shifting outside Europe.

According to analyses by Plastics Europe, although the global situation has improved, the data for Europe are far less encouraging. Reports indicate that in the first quarter of this year, average industrial production across Europe fell by 1.7% year on year. Industrial output increased in two of the five largest EU economies (Germany and Spain), while in the other three (France, Italy and Poland) declines were recorded.

It is not only energy-intensive sectors but also many other industries that are struggling with falling orders. EU production of plastics in primary forms in the first quarter of 2024 rose by 2.7% compared to the previous quarter. It was also higher than a year earlier, but demand was driven mainly by orders from outside Europe. Current production levels remain around 20% lower than before the outbreak of the war in Ukraine.

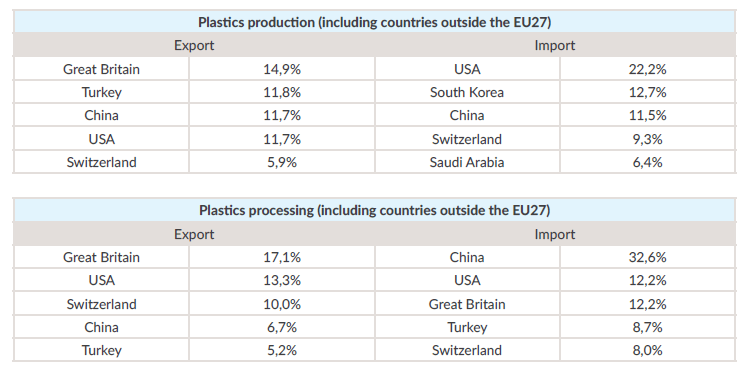

Non-EU trading partners (in terms of sales value) in 2023. Source: “Plastics in the circular economy. Analysis of the situation in Europe”, Plastics Europe 2024

If this trend continues, Europe will be forced to import raw materials and products from third countries – a move which carries not only price risks but also political risks. The earlier dependence on Russian raw materials, or today’s reliance on imports from the United States, demonstrates how dangerous it can be to rely on sources over which Europe has little real influence. With regard to trade in plastic products, the risk of political relations with the US having a major impact appears smaller, owing to the relatively modest export surplus over imports.

Not only producers but also plastics processors in the EU are failing to see growth. Since 2023, there has been a decline in the value of goods sold by EU companies on the internal market. At the same time, since 2022, production of plastic products has also fallen. Nevertheless, the EU has maintained a relatively stable positive trade balance with non-EU countries. Declining demand within the EU market is being partly offset by exports.

Pressure to recycle – sound assumptions, difficult practice

EU policy assumes the intensive development of recycling as one of the pillars of the circular economy. This direction is undoubtedly correct – increasing recovery and reuse of plastics can, in the long term, deliver tangible environmental and economic benefits. The problem arises, however, when significant volumes of recyclate from outside the EU begin to enter the market. Imported material is often more competitive on price, but its quality does not always meet the EU’s strict standards. The absence of effective mechanisms for verifying and controlling the technical parameters of recyclate from third countries risks undermining confidence in the entire secondary raw materials segment. At the same time, imports of cheaper recyclate weaken the competitiveness of local plants, which continue to struggle with surpluses of their own waste and limited options for managing it.