Between 2018 and 2025, the secondary market for extrusion-blow molding machines for PP, PE and PVC evolved through sharp cycles shaped by the pandemic, shifting end-use needs and uneven asset availability. According to MachinePoint data, demand was highly concentrated on a handful of brands and the most productive size classes, whereas supply was more dispersed across manufacturers and models. This mismatch influenced time-to-sale, with equipment from favored brands and configurations changing hands faster than less sought-after alternatives. The inflection point came in 2020, when sanitary packaging demand spiked and requests for used lines surged. A subsequent slowdown in 2021 and a collapse in 2022 gave way to renewed strength in 2023 and 2024, with 2025 tracking toward recent highs. By contrast, available stock fluctuated erratically, tightening drastically in 2020, rebounding strongly in 2022 and easing again thereafter. Across the period, buyer preferences trended toward electric, automated and energy-efficient plants, and toward machines up to 10 liters, with parallel but less pronounced interest in up to 2 liters units. Regional trade flows reflected established plastics hubs, with Europe, and Italy in particular, leading global supply.

Brand dynamics amplified these patterns. Magic consolidated a leading position that aligned with demand for electric and efficient systems, while Uniloy, Bekum and Kautex sustained the presence of historic names. Automa and Meccanoplastica provided consistent alternatives. On the supply side, the mix was broader and included a growing, though still limited, stream of machines from Chinese manufacturers. Resulting imbalances, observed by brand and by machine type, underpin recurring gaps between what buyers seek and what sellers can offer at a given time.

Demand and supply cycles in 2018–2025

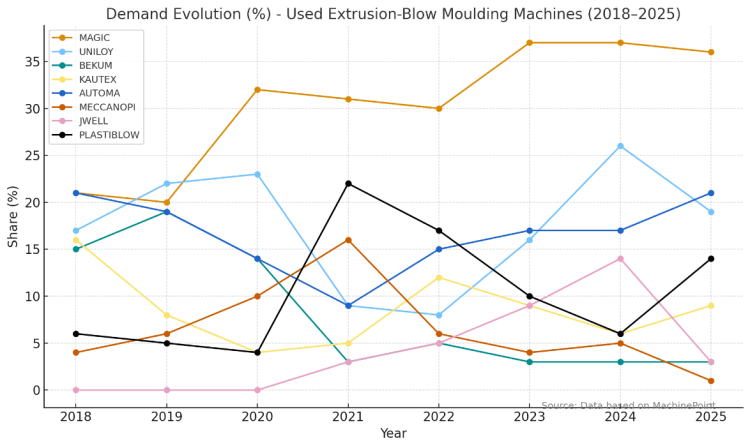

MachinePoint reports that the demand trend was non-linear. The turning point arrived in 2020, when the pandemic triggered a surge in sanitary packaging and pushed requests to unprecedented levels. After cooling in 2021 and collapsing in 2022, demand recovered in 2023 and 2024, with 2025 data anticipating year-end at recent highs.

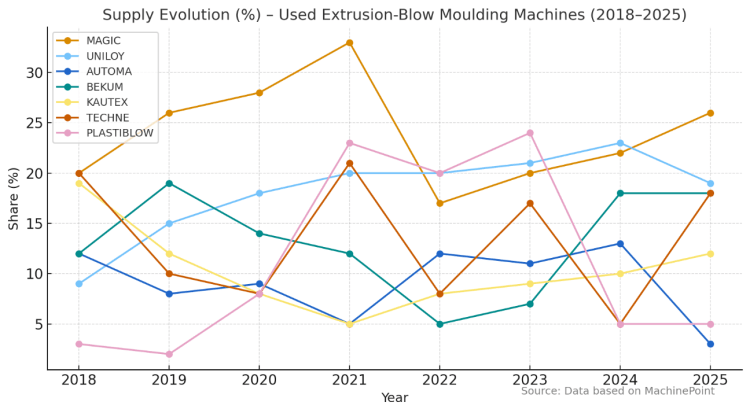

Supply followed a different cadence. After growth in 2019, availability collapsed in 2020, then rebounded strongly in 2022 before declining again in subsequent years. The result was a market oscillating between scarcity and sudden abundance, complicating procurement for specific brands and configurations and widening bid-ask spreads in tight phases.

Brand dynamics in the secondary market

Italian manufacturer Magic emerged as the primary reference, reaching up to one quarter of demand in 2020 and retaining about 16 percent in 2025. This leadership reflects buyer preference for electric, automated and efficient plants. Uniloy, Bekum and Kautex maintained the relevance of historic brands, while Automa and Meccanoplastica provided steady, though less consistent, alternatives.

On the supply side, concentration was lower. Magic, Uniloy and Automa were regularly present, yet their individual shares seldom exceeded 20 percent. Bekum and Kautex appeared less frequently. In recent years, Chinese manufacturers began to surface in supply, but with a limited role. Overall, what buyers seek does not always match what is available, reinforcing time-to-transaction disparities across brands.

Machine types and technology preferences

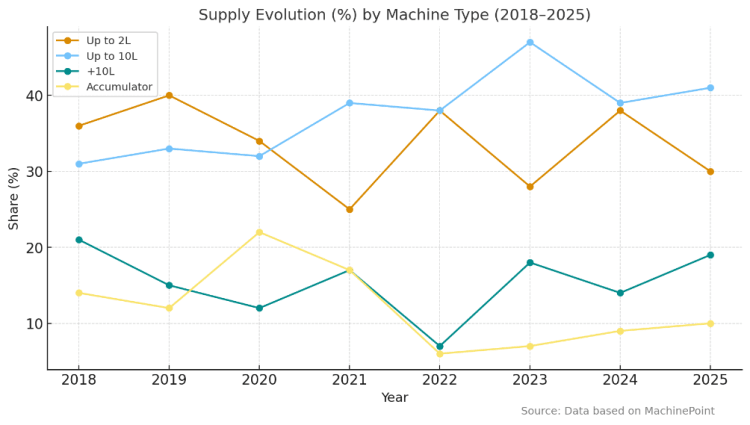

By machine type, the imbalance remained visible. Accumulator head machines sustained demand around 10–15 percent, with supply not fully aligned. Large-container machines recorded a temporary peak in 2020, then retreated to much lower levels. The core of the market was machines up to 10 liters, typically exceeding one third of demand, while supply was clearly insufficient. Smaller machines up to 2 liters followed a similar path with a 2020 peak, driven by the boom in single-use bottles for hydroalcoholic gel during the pandemic.

Technology preferences reinforced these shifts. Full electric plants showed growing demand in line with lower energy consumption targets and higher production efficiency, making them an increasingly favored option across applications.

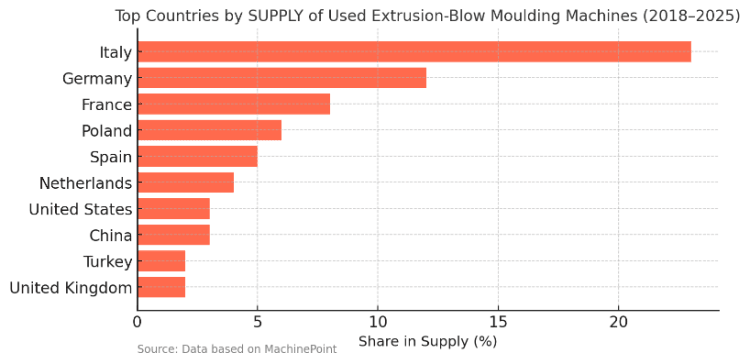

Geographic distribution of demand and supply

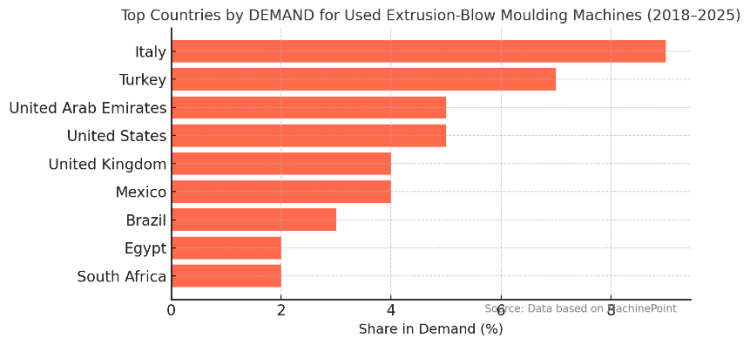

Trade flows were uneven and mirrored industrial bases and local market conditions. On the demand side, Italy accounted for roughly 8–10 percent, confirming its position as a European plastics hub. In the Middle East, Turkey and the UAE each held about 5–7 percent. In mature markets, the United States and the United Kingdom registered around 4–6 percent apiece. In Latin America, Mexico stood out with about 3–5 percent, followed by Brazil. In Africa and other regions, demand was more fragmented, with focal points in Egypt and South Africa.

Supply traced a different map. Italy led clearly with about 20–25 percent of global supply, reflecting the origin of many leading brands and a high rate of plant turnover. Germany and France followed, together contributing roughly 15–18 percent, underlining Western Europe’s weight as a secondary-market source. Poland and Spain also stood out with stable shares of around 5 percent each. Outside Europe, the United States and China contributed about 3–5 percent each, while most emerging countries had marginal supply.

Outlook

The period under review highlights a structural pattern: demand concentrates on select brands, electric systems and sub-10-liter machines, while supply is more diffuse by origin and type. As long as these preferences persist and asset turnover remains cyclical, the market will continue to alternate between scarcity and abundance, with transaction speed favoring listings that align closely with buyer priorities.