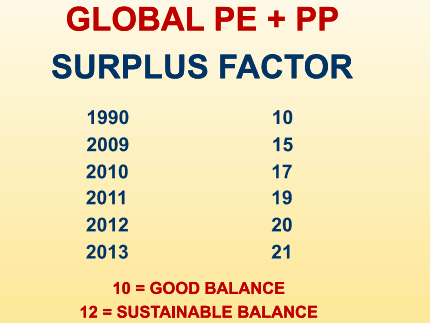

Scheidl demonstrated the dangers for producers through the use of the ‘surplus factor’ – nameplate capacity minus offtake, divided by nameplate capacity. A good surplus factor is 10, while 12 is sustainable, he said. And yet, overall, across PE and PP, it is almost 20 years since a 10 has achieved. The figure is already over 20, and could almost hit 40 by 2013.

Capacities totalling almost 50 million tpa are now at least 15 years old, and in some cases three times that, Scheidl noted. Their costs have been written off, and they could, theoretically, be shut down. “But sites die very slowly, if at all.”

Polyolefins surplus factor has not been sustainable for years (Source MBS)

Octene could supplant hexene as a comonomer

Peter Steylaerts, Linear Alfa-Olefins Regional Market Manager for Ineos Oligomers, gave an interesting presentation on current challenges in the polyethylene comonomer market. He indicated that with the current tightness in hexene that is due to last for many months, companies offering or using technologies that enable use of alternative monomers such as octene will be at an advantage. Demand for hexene is likely to out-strip supply until late 2011 at the earliest, Steylaerts said, whereas octene availability “is not an issue moving forward.”

Markus Gahleitner, IPR (intellectual property rights) Group Expert at Borealis, talked about the company’s Borstar PP for advanced packaging solutions. He cited two decisive elements: Borstar PP process technology and Sirius emulsion catalyst technology.“By combining a scientific and far-sighted approach to basic problems along the “chain of knowledge” from catalyst and process to modification and conversion with the intensive communications with customers and end users of our materials, it will be possible continue to expand the application range of polyolefins significantly,” Gahleitner said.

Logistics are increasingly important

As new polymer production centres emerge and expand, there is a growing need for improved logistics to move materials around plants, to and from shipping terminals and to customers. This year, PEPP devoted an entire session to the subject, with presentations from various players involved in the materials movement business.

Harald Wilms, Business Development VP at Zeppelin Silos & Systems, said that while the traditional model of polymer logistics has worked well within a single continent, where transport from the producer to the user could be done in virtually a single operation (mainly by truck in Europe, more by train in North America), extended distances between source and user soon require additional elements such as distribution centres, as well as specialist service providers. With intercontinental shipment, this is the norm.

Wilms outlined various storage and transport technologies available to close the link between the polyolefin producers and their clients in the downstream compounding and conversion industries. Discussing intercontinental shipment by bulk carrier, he said that with increasing capacities of polymer plants, their focus on few commodity grades per plant, and the export of these polymers to distant locations, new concepts may become economic in the future. “Any container ship can only be filled to a maximum of 2/3 with polymer containers,” he said. This problem can be overcome by using bulk carriers, similar to those known for bulk cargo shipments of grain or coal or minerals.

Toon Bruining, Group Supply Chain & Marketing Director at InterBulk Group, agreed that market developments are forcing the polymer industry to review existing supply chains. Over-capacity and volatile markets call for agile supply chains that are cost- and cash-efficient, he said. He also noted that multiple stock locations and divided responsibility for inventory management further increases stock levels.