Rigid plastics vs flexible

Rigid plastic packaging is under growing threat from flexible plastic pack formats. Over the last decade rigid pack formats across various end-use applications have been gradually replaced by flexible packaging types.The flexible packaging industry is promoting more of the ‘pre-cycling’ benefits of their packages versus rigid packaging as the combination of environmental pressures and uncertain polymer prices persist. Flexible packaging uses fewer resources and less energy than rigid polymer formats. This equates to significant reductions in packaging costs, materials use and transport emissions, as well as giving some performance advantages over rigid packaging.

Stand-up pouches, for example, are lighter-weight and have lower material use compared with rigid containers. The heat-resistant retort stand-up pouch is made of laminated plastic films, or foil, if microwaving is not required.

Pack designers are investigating new features, such as handles, and fixtures, such as child proof caps, to challenge rigid formats creating a corresponding desire for pack differentiation in the rigid plastic segment.

The figures

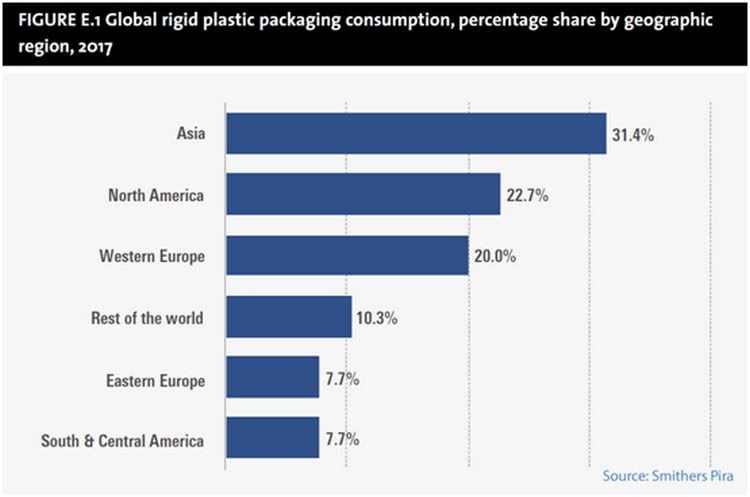

From a regional perspective, emerging economies are expected to grow rigid plastic packaging demand at the highest rates across 2017-2022.Asia is already the largest consumer of rigid plastic packaging, accounting for a projected 31.4% consumption share by volume in 2017. North America is the second largest consumer with 22.7%, followed by Western Europe with 20.0%. Asia is forecast to continue growing at a faster rate than any other world region with an annual average growth rate of 5.8% for the next 5 years.

Food is the largest end-use market for rigid plastic packaging, accounting for a projected 37.0% consumption share in 2017. The healthcare sector is forecast to grow at the highest rate, followed by other food markets, drinks and cosmetics.

Lifestyle and demographic influences

Demographic trends, translating into new demands and expectations of packaging are a key driving the selection of packaging formats. A high rate of population growth is more likely to be associated with growing packaged product consumption. The age structure of the population also plays an important role – for example ageing populations in advanced economies and better medical provision in developing countries will fuel increased demand for healthcare products.Lifestyle factors such as the rise of single-portion meals and on-the-go consumption can also favour lighter plastic formats, especially for small convenience pack sizes.

Full expert analysis on this fast-moving market can be found in The Future of Rigid Plastic Packaging to 2022. For more information, download the brochure here.

Source: Smithers Pira